The benefits of reinvesting your income distributions

Reinvesting the income distributions you receive from an ETF or managed fund can make a huge difference to your investment returns over time.

Owning units in exchange traded funds (ETFs) or managed funds that invest in shares generally gives you exposure to hundreds, and sometimes thousands, of different companies.

If you invest in fixed income ETFs or managed funds you’ll similarly be gaining exposure to a broad array of different bond issues.

Diversified funds invest across shares and bonds, so you’re gaining exposure to large ready-made portfolios made up of both types of assets.

Spreading your investments across different asset classes can help to reduce investment risk and also to diversify your sources of distributions.

One of the key advantages of investing in funds, apart from the potential capital growth you can expect over time, is that you’re also likely to receive regular income distributions.

That’s because funds typically receive company dividends (and fixed income payments if they invest in bonds), which are then aggregated and passed on to their individual unitholders.

The total amount of distributions you receive, which are usually paid quarterly, half-yearly or annually, will depend on the number of fund units you hold at the time the distribution payment amount is announced.

Making a choice

When you invest in a fund (whether it’s an ETF or a managed fund), you generally have two options when it comes to your income distributions.

You can your take them as cash, to spend as you like, or you can choose to reinvest them to buy additional units in the same fund. It’s completely a personal choice, depending on your circumstances and preference.

For many investors, especially those in the pension phase reliant on regular income streams, fund distributions are an important element of cash flow to pay for everyday living costs.

Other investors may not need additional cash income and are happy to build up their fund balance over time.

Reinvesting your distributions back into the same fund will increase the number of units you hold, which over the long term can compound both capital growth and income returns.

Comparing the options

There’s strong evidence that investors who consistently reinvest their distributions will likely achieve significantly higher investment returns over the longer term compared to those who choose to take their distributions as cash.

That reflects the compounding growth that can be achieved by having a higher investment balance. As your balance grows, so do your investment returns.

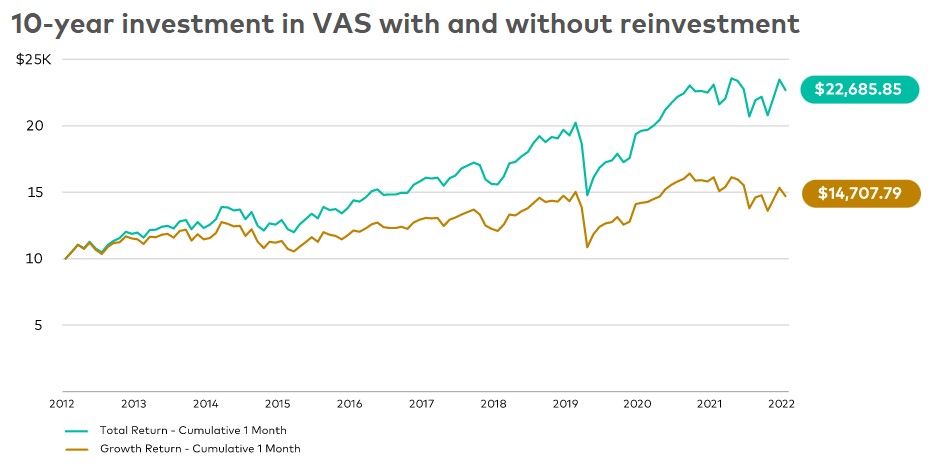

The chart below uses historical data and provides some good context around the solid investment growth achieved from reinvesting ETF income distributions over a 10-year period from 31 December 2012 to 31 December 2022.

It compares two hypothetical investors who each invested $10,000 into the Australian Securities Exchange-listed Vanguard Australian Shares Index ETF (ASX code VAS) at the end of 2012.

For their outlay, both investors purchased the same number of VAS units based on the prevailing market unit price at the time.

“Investor B”, represented by the brown line on the chart below, opted not to reinvest their regular distributions.

“Investor A”, represented by the green line on the chart, opted to automatically reinvest all of their VAS distribution payments over time into purchasing additional units in the ETF.

Source: Vanguard calculations. Calculations are based on a $10,000 investment into the Vanguard Australian Share Index ETF from 31 December 2012 to 31 December 2022. Total returns are before fees and taxes.

After 10 years, Investor B would have ended up with a total investment balance of just over $14,700, equal to a growth return of about 46 per cent.

They would have received around $5,600 of income distributions.

However, Investor A’s $10,000 investment on the other hand would have grown 127 per cent to over $22,600.

They would have received the equivalent income distribution value as Investor B.

However, Investor A would have ended up with almost 100 more fund units than Investor B after 10 years because of the fact that they had opted to reinvest their cash distributions into buying additional units.

Because of the compounding returns on having a higher number of fund units, they would have ended up with around $2,300 more than Investor B who opted not to reinvest their distributions.

That’s the power of compounding returns at work, which can simply be achieved by following a long-term distribution reinvestment strategy.

Source: