At Future Wealth Planners we believe every investment strategy and process should change when the facts change. But long-term wealth creation principles seldom do.

George Clason’s Richest Man in Babylon is still the world’s best personal finance book - it was written in 1926.

This page attempts to explain our investment philosophy at Future Wealth Planners, how that informs and guides our investment process, the way we think about creating wealth and building an investment portfolio, and how our model portfolios are created.

Good investing principles rarely change. Yet in the financial markets, the only constant is change. The best reporters and financial marketers cater to the change. But the wise investor understands the dangers of this transient appetite.

She or he will create robust mental models, processes and methods to avoid chasing the latest fads, fictions and fears.

The Future Wealth Planners investment philosophy

Our investment philosophy is what guides us through times of extreme uncertainty. It’s our ‘why’ for investing the way we do.

For many years we have worked with an investment philosophy that is the product of our experience and education. After many years of research, interviewing, reading, education and experience, we have come to believe that the best approach for long-term wealth creation incorporates the following fundamental principles/truths:

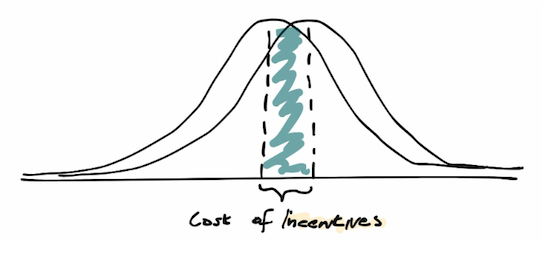

With these 10 principles considered, we believe it is possible for private investors to outperform the stock market over time - but given how hard it is, everyone should use passive index funds in the Core of his or her portfolio.

In our experience, the investors who produce exceptional returns tend to have high levels of intellectual humility and curiosity, always have a Plan B (the passive Core), always minimise taxes and fees, and only ever invest with optimism for the long-term.

The Core & Satellite approach

Our investment philosophy is about principles, backed by empirical research. Investment process is the ‘how’, using agile methods.

It’s how you express your investment philosophy and actually make money from investing.

We’ve met many investors, many of them far smarter than us, who do very poorly at investing. Why? We think it’s because most of them overcomplicate it.

As a result, we believe every investor will benefit immensely from following a simple and effective framework that’s been tried and tested for decades.

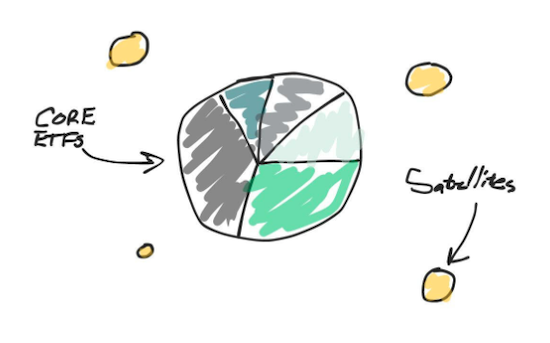

At Future Wealth Planners, we ask all our clients to consider using a ‘Core’ and ‘Satellite’ investment process for long-term wealth creation because it is simple, intuitive, limits risk, reduces envy and, of course, provides lots of long-term upside.

We have designed our Future Wealth investment portfolios to reflect this framework for investing, not just in shares/equities but across other asset classes as well.

It starts with the Core

The ‘Core’ of a portfolio is the centre of every investor’s universe. It’s where most investors should begin (and end) their investment journey.

We believe the Core of a portfolio should be reserved for investments that are:

In practice, index fund ETFs, property, and some managed funds go in the Core of our portfolios.

Satellite positions

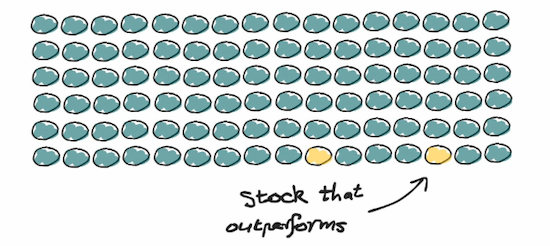

The Satellite part of a portfolio is the smaller part (or parts) that investors can reserve for their ‘active’ investing and higher risk positions.

We believe long-term time horizon (10-20+ years) and a high-conviction approach, driven by deep research and valuation work, are essential for success.

In our opinion, if the only reason you buy individual shares is to get wealthy over decades – we’re willing to bet you’ll be better off index funds, ETFs and managed funds. In our experience, investing in individual stocks in any meaningful way should only be considered by investors with extensive investing experience, time and curiosity.

How we identify which investments to buy

To identify individual positions (i.e. ETFs or managed funds), our approach can be summarised is as follows:

Additional notes

At a much deeper level, here’s what we will do day-to-day: our investment committee team will conduct full qualitative and quantitative reviews of investment opportunities using an in-depth proprietary framework. For example, we have access to a well-rounded quantitative and qualitative framework.

Generally an analyst from Bellmont Securities leads this, then the investment committee reviews and debate the suggestion as a team. The Independent Chair has the final say on whether a position is added to the models and has the responsibility of seeking feedback from the investment committee before a trade is ordered.

All important elements of our research are surfaced and presented to our clients, demonstrating our knowledge and the depth of our research - regardless of whether the investment will be made in our portfolios. For example, let’s say we review the ASX’s top dividend shares for harvesting franking credits for an income-focused portfolio. We might identify our top two ‘expressions’ (see below) but ultimately believe it is not the opportune time for us to invest. So, we will securely store that research in our cloud-based drives and share a comprehensive write-up of what we found with our end-investors. This builds accountability, transparency and flexibility.

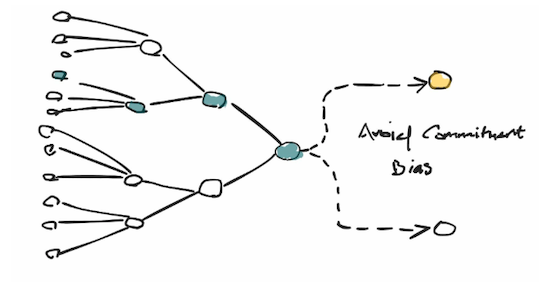

“Best expressions” principle

Our process day-to-day also has a logical ‘flow’, following the same principles above, but it will vary depending on which of the three investment types we are considering: shares, actively funds, or index funds. However, our team will also look ‘laterally’ for what we call the “best expression”. For example, within an asset class, we won’t simply compare blue chip share #1 against blue-chip share #2. Or ETF #1 against ETF #2.

We will seek to find the ‘best expression’ of every trade: whether it’s a diversified index fund, dividend ETF, thematic or sector exposure, LIC, REIT or active fund. For example, if we set out searching for tax effective income from ASX shares, we may end up concluding that the best expression of that trade (tax effective income) is actually to use an index fund. Or a LIC. Or REIT. This ensures we have a process roadblock before every portfolio decision, requiring us to stop, reflect and avoid the tunnel vision which often results in investors being blindsided. It’s also a great way for us to continually act in the best interests of our community.

If you would prefer to dig deeper into our philosophy and process, the following resources should help:

Future-Wealth-30-Portfolio.pdf

Future-Wealth-40-Portfolio.pdf

Future-Wealth-50-Portfolio.pdf

Future-Wealth-70-Portfolio.pdf

Future-Wealth-90-Portfolio.pdf

--------

Receive news updates, special offers and exclusive invitations to seminars and events.